This Week in Retirement: Economic Signals, Tax Moves, and What They Mean for Your Future

As a retirement-focused advisor with CFP® with a passion for the psychology of finance, my passion is helping you interpret the flood of economic news into clear, practical action for your best life. Here’s what caught my eye this week—and why it matters for your retirement.

The Price Hike "Lag" – Why Tariffs and Wars Don’t Hit Overnight

“There is typically a delay of between 90 and 120 days before changes in cost of raw materials impact our cost of products sold.” – WD-40 earnings call.

Source: WD-40 Company Q2 2026 Earnings Call Transcript

Commentary:

If international tensions or tariffs hit the headlines, you have a brief window before costs pass through to you. Retirees should use these windows wisely—review spending, replenish cash accounts, and avoid big-ticket purchases if you suspect a rise is coming. This “delay effect” isn’t an excuse to panic—it’s a chance to plan ahead.

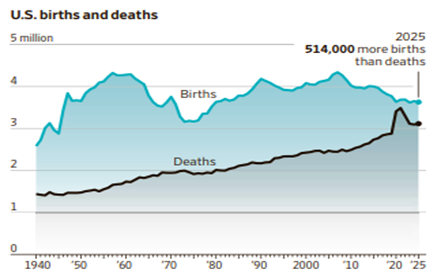

When Births Cross Deaths: Demographic Destiny Ahead

Data shows US births and deaths on a path to cross, with profound, long-range economic implications.

Source: U.S. Census Bureau – Births and Deaths Projections

Commentary:

An aging population means fewer workers, slower economic growth, and more pressure on Social Security and health care. For retirees, this underscores the importance of creating sustainable income streams, delaying Social Security when possible, and maintaining flexibility in spending to weather any future benefit changes.

Inheritance Isn’t a Retirement Plan

42% of heirs age 50+ had their net worth fall to/below pre-inheritance levels within one year of receiving an inheritance (Texas Tech/University of Alabama study).

Source: Texas Tech University Research

Commentary:

This reminds us that windfalls rarely “solve” retirement. Without a plan and financial discipline, inheritances can vanish quickly. The key for retirees: focus on sustainable, intentional spending and ongoing planning over “one-and-done” windfalls.

Cash Sales Up: What’s in the Earnings?

Delta Airlines reports, “Over the last month, cash sales, which are the clearest indicator of demand, are up double digits.”

Source: Delta Air Lines Q1 2026 Earnings Call Highlights

Commentary:

Robust cash sales show consumer demand is strong—often meaning economic fundamentals remain sturdy, at least for now. Retirees can use these “real world” clues (not just headlines!) to gauge the climate for spending, travel, and portfolio adjustments.

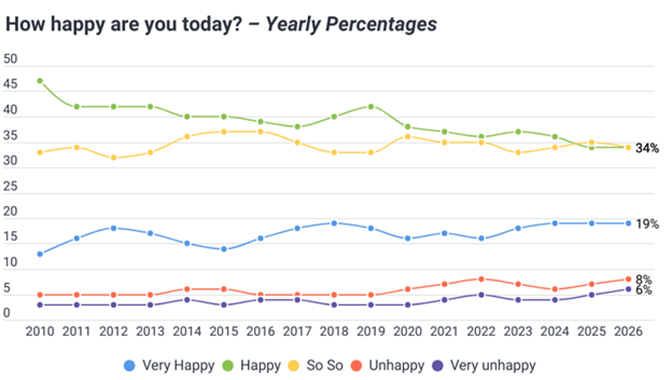

Measuring Real Happiness: A Sentiment Survey Worth Watching

The “How Happy Are You Today?” survey has polled 1.5 million Americans daily for 16 years, offering unique insight into sentiment and well-being.

Source: Gallup U.S. Mood Index

Commentary:

True retirement satisfaction is about more than your portfolio—it’s about your perceived happiness and well-being. Tracking sentiment reminds us to emphasize not just wealth but purpose, relationships, and health. Align your spending and lifestyle with what brings lasting happiness, not just financial security.

Small Policies, Big Ripples: Local News, Global Change

A Massachusetts town rejected a 50% property tax hike for more efficiency; Maine banned new large data centers—both could shape nationwide trends.

Source: Boston Globe: Tax Hike Vote, AP: Maine Data Center Ban

Commentary:

Property taxes and infrastructure directly affect retirees’ fixed costs and home values. Keep an eye on local policy—sometimes the biggest threats (or opportunities) to your retirement come from your state or town, not Washington.

Gen Z & Parental Support: Trickle-Down Pressure

64% of Gen Z adults (ages 18-28) rely on parent support; 56% of their parents say this strains their own finances (Wells Fargo 2026).

Source: Wells Fargo 2026 Money Study

Commentary:

If you’re supporting adult children or grandchildren, remember: generosity should have guardrails. Make sure your retirement is secure before “helping” to the point of strain. A solid plan allows you to assist family—without sacrificing your lifestyle or peace of mind.

Who Really Moves the Market? Presidential Scorecard

See S&P 500 performance across the last four presidencies.

Source: Financial Times

Commentary:

Presidents get too much credit (or blame) for market returns. The lesson for retirees: don’t make drastic investment changes tied to elections or political cycles. Stick to your long-term plan, review it periodically, and avoid knee-jerk reactions around election years.

The Real IRS Math: Who Pays What?

Despite popular belief, the top 1% pay an average federal tax rate of 23%, versus 14% for all Americans and 3.75% for the bottom half.

Source: IRS – Federal Income Tax Data

Commentary:

Understanding who really pays what can inform tax planning. Retirees with high assets should proactively manage tax brackets and consider Roth conversions or charitable giving to add flexibility and control over lifetime taxes.

How the Wealthy Will Cut 2026 Tax Bills

WSJ reports the top five tactics:

- Long-short tax-loss harvesting

- Bonus depreciation

- Changing domiciles

- Bunching charitable gifts

- Opportunity zones

Source: WSJ: Savvy Wealth Tax Moves

Commentary:

Many of these tools can work for retirees, too! You don’t have to be ultra-wealthy to benefit from “bunching” charitable gifts, harvesting losses strategically, or considering a move to a lower-tax state. Discuss these tactics with your advisor before year-end to maximize your own after-tax retirement income.

Final Thoughts

This week’s news underscores a core retirement truth: Thriving is less about reacting to headlines and more about preparing with flexibility, awareness, and purpose. Whether costs are rising, inheritances vanish, or family pulls at your wallet—clarity, planning, and ongoing education are your best defenses and greatest growth tools. Align your resources to your life, not the other way around, and you’ll set yourself up for peace of mind and lasting satisfaction.