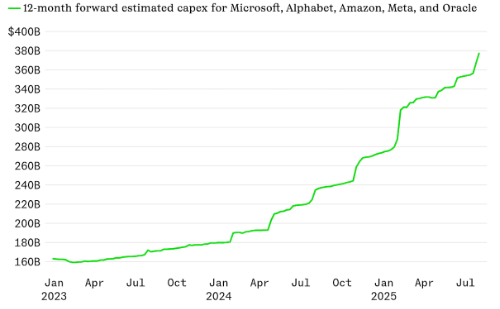

Probably the most exuberant takeaway from earnings season is the AI capex spending by companies. $80b already from MSFT alone. And it’s only the beginning.

Source:

Microsoft earnings report; Bloomberg Tech (2025)

Why it matters:

This shows how transformative AI is becoming in corporate strategy and capital allocation. For investors, it signals a long-term growth engine that could reshape productivity, profitability, and stock valuations across entire industries. For retirees, however, the lesson is two-fold: AI may present growth opportunities in portfolios, but it also underscores that markets will continue to evolve in unpredictable ways. Diversification and risk management remain critical, since today’s hottest growth trend could become tomorrow’s bubble.

The Society of Actuaries (SOA) reports one in three pre-retirees are financially supporting adult children and caring for aging parents.

Source:

Society of Actuaries (SOA, 2025)

Why it matters:

This is one of the most overlooked risks to retirement plans. If you’re helping both generations financially, your nest egg may be stretched much thinner than you anticipated. For high-net-worth households, these obligations can quietly drain capital that was earmarked for travel, healthcare, or estate goals. Building a flexible income plan and setting boundaries around support can help protect your long-term financial security while still caring for family.

A fun quick one… Nvidia IPO’d at $12 in 1999.

Source: Bloomberg Markets (1999–2025)

Why it matters:

This is a reminder that innovation and patience can create massive wealth. But it’s also a cautionary tale: most people didn’t hold onto Nvidia from the beginning, and many similar “next big things” never pan out. Chasing the next Nvidia often leads to disappointment. The better path for retirees is to capture broad exposure to innovation while keeping the majority of assets in strategies aligned with preserving and producing income.

31% That’s how much higher the average net worth of millennials and older Gen Z members was in 1H 2025 than boomers at similar ages.

Source: Federal Reserve (2025 H1 data)

Why it matters:

Younger generations are building wealth faster than prior ones, largely due to real estate gains, market appreciation, and rising wages in tech-driven industries. For retirees, this has estate planning implications: heirs may not need as much direct financial support, but they may face different risks (like overexposure to market volatility). Aligning your estate, tax, and gifting strategies with your heirs’ actual circumstances can make your wealth transfer more impactful.

With the GENIUS, Anti-CBDC Surveillance State, and CLARITY acts, interest in Crypto investing has a new green light. Soon we will see investment options in annuity and life products. Already available in structured products.

Source: U.S. Congress Acts (GENIUS, Anti-CBDC Surveillance State, CLARITY, 2025)

Why it matters:

Crypto is no longer just a fringe investment—it’s finding its way into mainstream retirement vehicles. That means your children and grandchildren may adopt it in their financial lives, and you may soon be asked if it has a place in yours. Whether you use it or not, understanding the regulatory landscape and how it may fit (or not) in a retirement portfolio is critical. Staying informed keeps you from being caught off guard by a fast-moving market.

The number of people unemployed for at least 27 weeks has topped 1.8mm. The highest level since 2017 sans Covid.

Source: U.S. Bureau of Labor Statistics (2025)

Why it matters:

Prolonged unemployment puts strain on the economy, reduces consumer spending, and creates political pressure. For retirees, this matters because it can affect everything from Social Security solvency to market confidence. In a more immediate sense, it reminds us that family members may face sudden job insecurity, and you may be called upon to help. Preparing for these possibilities in advance ensures your retirement plan stays resilient.

Vanguard just changed its recommended portfolio mix to 70% bonds and 30% stocks. The reasoning is simple: valuations.

Source: Vanguard (2025)

Why it matters:

You may have seen Vanguard’s latest recommendation to shift retirement portfolios toward 70% bonds and 30% stocks. On the surface, that sounds safe — after all, bonds are supposed to be more stable. But here’s the problem: bonds carry their own risks, especially in today’s environment. Inflation can quietly eat away at your purchasing power, and if interest rates move unexpectedly, bond values can drop.

What this tells me is that many investors will be steered into strategies that may feel comfortable in the short run but could actually limit their ability to grow over the long run. My approach is different. Instead of simply following a one-size-fits-all model, I help you build a retirement income plan that balances growth with protection — designed around your actual goals, not just broad market assumptions.

761 million. That is the number of 2Q Doordash orders. A new record.

Source: Doordash Q2 2025 earnings

Why it matters:

Beyond being a fun stat, it shows how consumer behavior has shifted toward convenience-first spending. For retirees, this reinforces two realities: costs of living continue to evolve in ways that weren’t modeled in traditional retirement planning, and investing in companies that benefit from these shifts can be rewarding. It’s also a reminder that financial strategies must adapt as quickly as consumer habits do.

It’s been a while since I put out this chart. Through June.

Source: Peter Mallouk, Creative Planning 2025

Why it matters:

How do you combat the devaluation of your dollars, otherwise known as inflation!? This is the ultimate question for retirees living on fixed income and should be one of the primary concerns of a well laid out plan. Income should increase as time passes, your money should be invested and growing, and larger portfolios should recognize the unique power of gold in their portfolio. It is a fantastic currency hedge as well as a low correlation diversifier to the typical stocks and bonds.

Rent not own. The share of renters 65 and older rose 30% in the past decade.

Source: Harvard Joint Center for Housing Studies (2025)

Why it matters:

Housing is one of the largest drivers of retirement expenses. Renting may free up capital, reduce maintenance headaches, and provide flexibility, but it also creates uncertainty about rising costs. For retirees, the decision to rent vs. own is not just financial but deeply tied to lifestyle, healthcare access, and legacy planning. Advisors should encourage clients to revisit this decision regularly rather than assume their housing strategy is “set for life.”

We will see increases in auto insurance because of tariff impacts on repair costs. The national average being 7%. 7% increase is 7% of retirement spending.

Source: Insurance Information Institute (2025)

Why it matters:

This is more than an annoying bill increase—it’s a direct hit to retirement budgets. A 7% increase in auto insurance may not sound like much, but it compounds with healthcare, housing, and food inflation. These “everyday” cost increases are often the silent killers of retirement plans. Factoring in lifestyle inflation into spending projections is essential to avoid surprises down the road.

Final Thoughts

This week’s themes highlight a clear truth: retirement planning isn’t just about markets, it’s about life. From AI-driven corporate spending to the rising costs of insurance, housing, and family obligations, retirees are navigating a constantly shifting landscape. The key is flexibility—your portfolio, your income plan, and your estate strategy must adapt as quickly as the world around you. Wealth in retirement is not just about preserving assets, but about sustaining confidence and freedom in the face of change.