This Week’s Retirement Insights: Wealth, Rates, Risk & Real-Life Desicions

The Great Wealth Divide: Lifespan Gains for the Wealthiest

The Economist reports the richest 1% of American men live almost 15 years longer than the poorest; for women, the gap is 10 years.

Source:

The Economist – Wealth & Longevity

Commentary:

The correlation between wealth and longevity isn’t just about being able to afford better healthcare. It points to the cumulative benefits of long-term financial stability: reduced stress, access to preventative services, healthier living environments, and the ability to nurture meaningful social connections—all associated with healthier, longer lives. As your advisor, my mission is to help you build not just financial security, but a holistic foundation for well-being. We focus on strategies that enhance your quality of life over decades, such as regular health screenings, social engagement, and purposeful living—all possible through thoughtful financial planning.

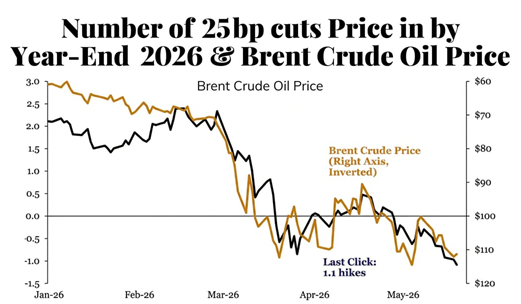

From Rate Cuts to Possible Hikes: Interest Rate Expectations Shift

Earlier this year, markets expected over 60bps of rate cuts. Now, there’s a 40% chance of hikes as energy prices tie closely to inflation.

Source:

Bloomberg – Fed Rate Outlook

Commentary:

Interest rates have an outsized impact on retirement planning—affecting everything from investment returns to mortgage costs, and from fixed income yields to how businesses borrow and invest. We’re seeing greater uncertainty due to the link between energy prices and inflation. This means your retirement portfolio must be resilient: having enough liquidity for lifestyle needs, exposure to growing sectors, and a mix of assets that stand up to both inflation and rate hikes. Together, we review and adjust your income strategy, keeping your plan flexible and ready to thrive regardless of what central banks do next.

Summer Travel Spending Rises

66% of surveyed summer travelers expect to spend more this year than last, according to Bloomberg.

Source:

Bloomberg – Summer Travel Survey

Commentary:

Travel and experiences are what make retirement meaningful—but rising costs can be a source of anxiety. My advice is to budget intentionally for leisure and adventure; these memories are as valuable as any portfolio line item. Through ongoing planning and regular check-ins, we help you prioritize experiences, navigate travel deals, and maximize your enjoyment without threatening long-term financial stability. We also look at ways to use rewards and points, and discuss travel insurance and healthcare access abroad—so nothing stands between you and your next adventure.

Housing Costs Consuming More Income

The Burns Affordability Index finds homebuyers now allocate 42% of their incomes to housing (based on 10% down on a median-priced home).

Source:

Burns Affordability Index

Commentary:

Retirement housing decisions often define financial comfort well into the future. High housing costs can reduce your ability to fund other priorities, travel, or healthcare. Whether your goal is to age in place, downsize, or relocate, we assess your total cost picture—including taxes, maintenance, and future care needs. I use scenario planning to show how various housing choices affect your cash flow, equity, and overall financial confidence, so you can decide on a home you love and a lifestyle you can afford.

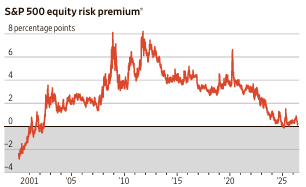

Equity Risk Premium Approaches Historic Lows

The S&P earnings yield vs. the T-10 rate (Equity Risk Premium) is near the lowest since 2000.

Source:

Morningstar – Equity Risk Premium

Commentary:

This metric helps us gauge whether stocks offer enough reward relative to bonds. With premiums at historic lows, it’s critical for retirees to avoid being overly optimistic about stocks or fearful of missing out. Diversification is our defense—knowing when to tilt towards bonds for stability and when to allow for growth. I help you review your asset allocation regularly, ensuring your income needs are met with the least amount of risk, and that your investments adapt as the market environment changes.

Cybersecurity Tops Risk Concerns

77% of leaders from 500 large/mid-sized companies say cybersecurity is their top risk concern.

Source:

WSJ – Cybersecurity Risk Survey

Commentary:

Online threats aren’t reserved for big businesses; retirees are increasingly the targets for scams and identity theft. Protecting your accounts, privacy, and assets is now as important as protecting your physical health. We make cybersecurity an ongoing part of our planning: from regular fraud checks and password audits, to helping you identify potential phishing attacks. A secure digital life is a foundation of your financial wellness, and I provide tools and guidance to ensure you are protected.

Advisors Expand ETF Use: Average Portfolio Holds Nearly 90 ETFs

RIAs keep adding ETFs, holding an average of 89.7 per firm in Q1.

Source:

ETF.com – Advisor Portfolio Trends

Commentary:

ETFs often provide greater flexibility, lower fees, and exposure to innovative asset classes. But complexity can sometimes add confusion. My approach: simplicity and purpose. We use only what supports your goals, and I make sure you understand exactly what you own—avoiding unnecessary overlap and ensuring your investments stay aligned with your risk tolerance and cash flow needs.

Financial Transparency Lacking Before Cohabitation

70% of people admit they didn’t know their partner’s full financial situation before moving in together.

Source:

MarketWatch – Financial Transparency Study

Commentary:

Retirement planning is often a “team sport.” Whether you’re married, partnered, or preparing for solo living, understanding each other’s financial foundation is essential. Financial transparency isn’t always easy, but it leads to greater confidence, fewer surprises, and a smoother transition through retirement’s milestones. I provide resources and facilitate candid conversations, helping couples align values, clarify goals, and build a unified plan that supports both partners’ needs.

Bear Market Fears: A 35% Decline Would Erase $23 Trillion

A 35% US stock market decline (bear market territory) would wipe out $23 trillion in wealth.

Source: Barron's – Bear Market Impact

Commentary:Large declines can have a real psychological and financial toll, especially for those relying on their investments for income. But with proper planning—including cash reserves, protected income strategies, and regular risk reviews—we prepare not just for the market’s best days, but its worst. I use stress-testing and “what if” scenarios so you feel confident your lifestyle won’t collapse if markets stumble. This is how we transform worry into preparation.

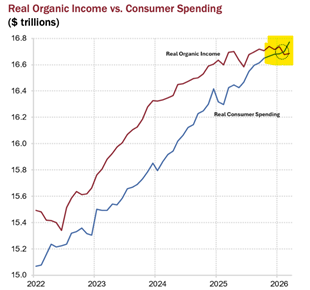

Consumers Are Spending More Than They’re Earning

Charts show real organic income vs. real spending: Americans now spend more than they earn, excluding government transfers.

[real organic income = real personal income excluding gov handouts]

Source:

Federal Reserve – Consumer Spending Report

Commentary:

Spending outpacing income is concerning, particularly for retirees with a fixed or slowly growing nest egg. We focus on sustainable withdrawal strategies, realistic budgeting, and regular reviews to ensure your resources last through all retirement stages. Sometimes, lifestyle adjustments or creative solutions can make a big difference. My job is to make this process clear, honest, and empowering—not restrictive.

Car Loan Payments of $1,000+ Become Commonplace

Experian finds 19% of 5+ million car loans come with payments of $1,000/month or more—74% are non-luxury trucks, up from 5.4% five years ago.

Source:

Experian Car Loan Study

Commentary:

Major debt in retirement can threaten cash flow and erode financial flexibility. We review every big expense together: weighing the pros and cons, understanding total costs, and considering alternatives such as downsizing, leasing, or pre-owned vehicles. Your plan supports not just your transportation, but your peace of mind.

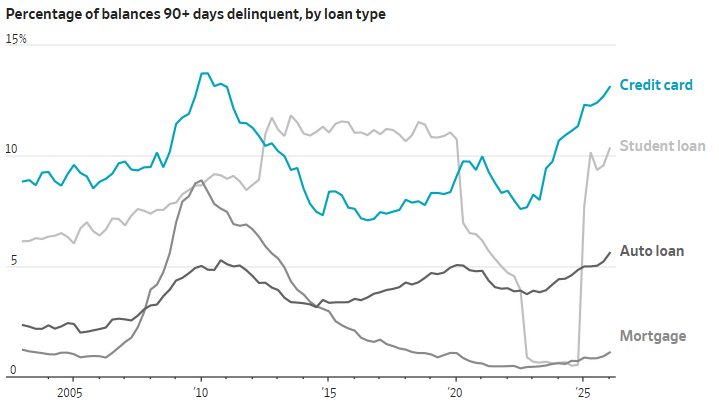

Loan Delinquency on the Rise

Experian reports increasing rates of 90+ day delinquency—especially on credit cards and car loans.

Source:

Experian Consumer Credit Report

Commentary:

Managing debt is essential to protecting your credit score, minimizing stress, and keeping your options open in retirement. Regular credit reviews, attention to payment histories, and proactive strategies to reduce debt are all part of our holistic approach. We cover not just investments, but your entire financial picture.

Final Thoughts

Retirement is about more than growing assets—it’s about using them wisely for a fulfilling, resilient life. This week’s news underscores the need for thoughtful, ongoing planning: Whether it’s the longevity gap, shifting interest rates, rising travel and housing costs, market volatility, cybersecurity threats, or debt trends, each headline is a lesson in what matters most—adaptability, transparency, and education.

My role is to help you filter out noise and focus on meaningful strategies that support your values, dreams, and wellness. By integrating health, relationships, risk management, and intentional spending, we create your personal blueprint for retirement success. Preparation doesn’t mean perfection—it means confidence in the face of uncertainty, and a plan that evolves as your life and the world around you change.

Let’s take your next step together, so your retirement delivers not only financial security, but joy, connection, and confidence—regardless of the headlines.