This Week in Perspective: What Retirees Should Know

Staying informed is key to thriving in retirement. Here’s a rundown of this week’s notable economic, investing, and retirement trends—and why they matter for your future security and peace of mind.

Gold: Love It or Hate It?

A “gold only” investor who started in 1980 would have just broken even last year, two decades into retirement.

Source: CNBC, Gold’s 40-year round trip

Commentary:

Gold is a classic diversifier, often touted as a hedge against turmoil. Yet, many haters love to cherry-pick their statistics to prove their point. As in all investing, timing and allocation matter—a portfolio with only gold severely lagged stocks in some time periods but it has also significantly beat stocks in others. In retirement, a blend of assets aligned to your cash flow needs and risk tolerance is far more effective than chasing a single asset fad, even one as shiny as gold. With many believing that inflation is coming, gold is simply a piece of the inflation hedge pie.

The Great States Divide: Income Taxes

In 2006, 15 states had income tax rates under 5%. By 2026, it’s 26 states. On the flip side, states with double-digit income tax rates grew from one to six, with more on the way.

Source: Tax Foundation, State Tax Changes 2026

Commentary:

Where you live in retirement can profoundly affect your net income. As states move in opposite tax directions, it’s more important than ever to evaluate your retirement location—not just for weather, but for taxes, healthcare, and long-term planning flexibility. A smart relocation or “tax migration” plan can improve your retirement budget without reducing your lifestyle.

Gas Prices Spike—and Inflation Follows

AAA reports gas prices jumped over $0.24 in a few days. Goldman Sachs says a sustained 10% oil price hike bumps overall CPI (including food and energy) by 0.28%.

Source: AAA, Gas Prices Surge, Bloomberg, Oil and CPICommentary:Rising energy costs ripple into everything from groceries to travel. For retirees, the biggest risks are not just headline inflation but how spikes in day-to-day expenses affect your planned withdrawals. Keeping a flexible budget and maintaining a cash buffer for these periods can help you ride out volatility without stress.

Markets and Crises: A Contrarian Silver Lining

50 major conflicts since the 1950s: US stocks dropped ~7% on average at the outset, but a year later, they recovered in 85% of cases with a median 7% gain.

Source: Ned Davis Research, Geopolitical Events & Stocks

Commentary:

Headlines spark fear, but history suggests resilience. For retirees, emotional investing is costly—panic selling during headline turmoil risks missing the “snapback” that often follows. Having a plan and sticking to it is almost always the best approach.

Oil Shipping Costs Rocket on Middle East Risk

Cost to ship 2 million barrels of oil from the Middle East to China hit $425,000/day—a record high, twice last week’s price. Some Chinese firms now label vessels as “China Owner” for safer passage.

Source: Reuters, Oil Shipping Costs Soar

Commentary:

Geopolitics matter—even if you’re not invested in oil stocks. When shipping routes are threatened, supply chains and investment markets feel the pinch. Retirees benefit by having globally diversified portfolios that limit exposure to regional shocks.

The Power of Low Inflation: Time’s Silent Thief

At just 3% annual inflation, $100,000 saved today is worth the equivalent of only $55,000 in 20 years.

Source: U.S. Inflation Calculator

Commentary:

Retirement is a marathon, not a sprint. Even modest inflation erodes purchasing power drastically over decades. Your income plan must account for rising costs through growth-oriented investments, inflation-adjusted withdrawals, or guaranteed sources that keep up with living expenses.

Hardship 401(k) Withdrawals Hit a Record

6% of workers took a hardship 401(k) withdrawal last year, compared to a pre-pandemic average of just 2%.

Source: Plan Sponsor, 401(k) HardshipsCommentary:More Americans are tapping retirement savings early—a red flag for financial vulnerability. For those nearing or in retirement, building and maintaining adequate emergency funds and a flexible spending plan are essential to avoid painful choices down the road.

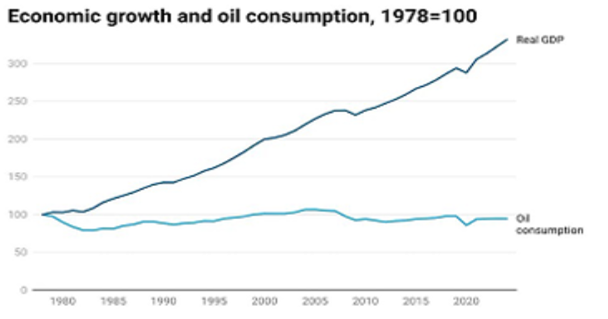

How Dependent is U.S. Growth on Oil?

Worries about oil prices are up, but America’s real GDP is less oil-dependent than in decades past.

Source: EIA, U.S. Oil Consumption & GDP

Commentary:

Economic growth is now more resilient to oil shocks, thanks to diversified energy sources and efficiency gains. Retirees benefit from market participation that embraces the broader economy, not just energy-dominant sectors, reducing the risk of overexposure to one driver.

Market Dips: Buy Opportunity Not Panic

Goldman Sachs says dips related to Iran or AI headlines should be seen as buying opportunities, not the start of a bear market.

Source: MarketWatch, GS Stock Commentary

Commentary:

Having cash or a plan for “dry powder” lets you buy when others are fearful. Successful retirees are disciplined contrarians—regular rebalancing or dollar-cost averaging means you may benefit from market volatility rather than be victimized by it.

Dubai: From Ultra-Safe to Flashpoint

Dubai attracted more millionaires in 2025 than any other country; 9,800 more expected in 2026-2027 despite new geopolitical risks.

Source: Henley & Partners, Millionaire MigrationCommentary:Global events can quickly change the fortunes of “safe havens.” Retiree portfolios should diversify globally, but also be monitored for political and currency risks, especially where new trends sound “too good to be true.”

“Whiplash” for Korea’s KOSPI Investors

South Korea’s KOSPI fell 12% in one day (largest in 20+ years), then gained 10% the next day (biggest jump in 18 years).

Source: Bloomberg, KOSPI Volatility

Commentary:

Wild swings highlight why emotional trading is so dangerous in retirement. Prudent investors use these events as reminders to stick to strategy, maintain diversification, and rebalance when appropriate instead of chasing headlines.

Prediction Markets: The Hottest (And Riskiest) Trend on Campus

Platforms like Kalshi and Polymarket are growing fast, pouring money into college sponsorships and encouraging students to “bet” on world events.

Source: WSJ, Prediction Market Craze

Commentary:

Gambling in disguise? These markets teach the wrong lessons about true investing: sustainable wealth is built over decades with discipline, not by gambling for a quick windfall. Retirees (and their families) should beware the allure of “easy money” and focus on proven wealth-building strategies.

Final Thoughts

Thriving in retirement is about much more than chasing return or dodging the latest crisis. It’s about knowing how to adapt to shifting markets, rising costs, changing tax policies, and global events—while always keeping sight of your unique vision for your best retirement.

Key takeaways for thriving:

- Diversify across assets and geographies.

- Have a thoughtful, written plan and revisit it regularly.

- Beware the seduction of headlines and fads; stick to proven, adaptive strategies.

- Consider where you live, how you spend, and why you invest—not just what headlines say.

- Lean on expert guidance when the landscape gets noisy.

Stay informed. Stay empowered. And remember: your retirement is a journey, not a destination—and the best journeys are planned with care, purpose, and a little bit of courage.