This Week’s Insights: Retirement Perspective on Markets, Innovation, & Opportunity

In investing, the biggest mistakes usually aren’t about buying the wrong stock. They’re about waiting until certainty replaces opportunity. - Howard Marks

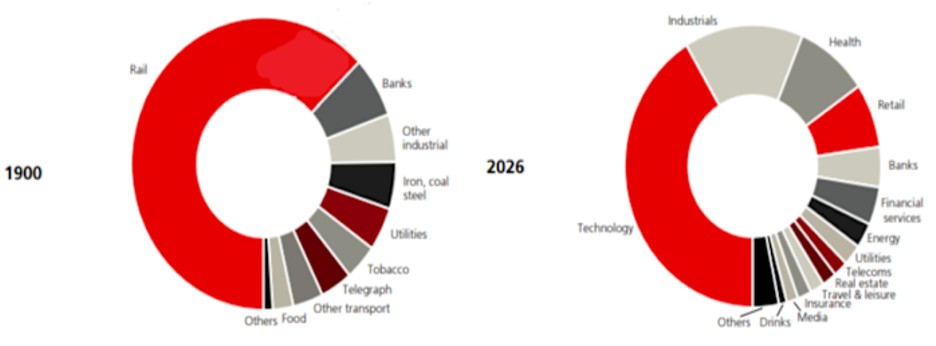

Market Concentration: The More Things Change...

If you think the market is overconcentrated now, consider 1900: nearly 50% of global equity was in Railroads, compared to today’s dominance by Tech.

Source: Visual Capitalist – History of Stock Market Concentration

Commentary:

Market concentration is nothing new. Every era has its “Magnificent 7”—but times and sectors change. For retirees, the lesson is diversification. The world’s next leader may not be today’s hottest sector. Anchoring your retirement to just one slice of the market can risk your lifelong income.

Stick with Tech? A Lesson in Discipline

An investor in US technology at the close of 1996, “irrational exuberance” and all, earned an annualized 14.1% through today; the overall US market, 10%.

Source: JP Morgan Long-Term Capital Markets Assumptions 2026

Commentary:

Even with doubts and pessimism, staying invested—especially in areas of innovation—can lead to outsized returns. In retirement, the key is not to chase fads, but to keep a disciplined allocation to growth sectors like tech, rebalancing to match your risk profile and withdrawal rhythm.

Crypto Joins the Financial Mainstream

Kraken became the first crypto exchange granted access to the Federal Reserve payments system—a first for digital asset dealers.

Source: Reuters – Crypto Exchange Kraken Taps Fed’s Payment System

Commentary:

Crypto is not just for the fringes anymore. While still volatile, regulatory acceptance means digital assets may take on a bigger role in everyday finance. For retirees, this is a “watch and learn” moment—don’t jump in, but pay attention to how mainstream innovation could eventually diversify or streamline your cash flow.

What’s Really Driving Inflation Right Now

Wednesday’s CPI: Sweetrolls, coffeecakes, and doughnuts up 3.6%. Beef up another 1.5% in a month, 14.5% year-over-year.

Source: Bureau of Labor Statistics – March 2026 CPI Release

Commentary:

Inflation isn’t just “up.” The composition matters! When staples like beef surge, your grocery bill feels the pain. Retirement plans must account for these spending shocks by building in inflation flexibility—either through rising income sources or targeted cash buffers for higher living costs.

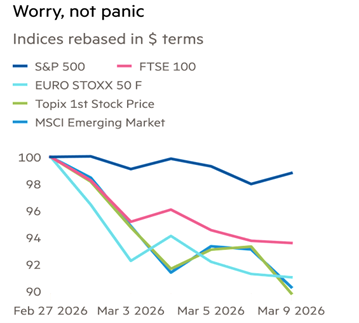

Markets in Wartime: Headline Indexes Can Deceive

Since the start of the War on Iran, major US indexes are down ~4%, but the average stock is down 18%.

Source: Bloomberg Markets – War Impact

Commentary:

Don’t let a “mild” market average lull you into complacency. Under the surface, many stocks are hurting far more than the headline number reveals. This reinforces the importance for retirees to hold diversified funds over single stocks—and to have a strategy that’s resilient even when headlines downplay risk.

Drones Change the Rules of Modern Warfare

The US sent 31 M1 tanks (~$10 million each) to Ukraine. 27 were destroyed or disabled by Russian drones costing under $1,000 apiece.

Source: CNN – Drones’ Impact in Modern Warfare

Commentary:

Disruption isn’t just financial—it’s global and technological. Just as cheap technology now overcomes the most expensive old guard in warfare, new innovations can upend traditional companies in your portfolio. Retirees should keep a balanced exposure to innovation and “defensive” holdings.

International Stocks Outperform US

Since last January, investors in non-US developed stocks returned 2.5x more than those in the S&P 500.

Source: MSCI EAFE Index Returns, Yahoo Finance

Commentary:

It’s easy to focus just on US stocks, but diversification abroad often pays, especially when the US is struggling or lagging. Retirees should consider keeping a portion of their portfolio in international equities for smoother returns and new opportunity.

Tapping into Home Equity

Today, Americans hold about $22.5 trillion in accessible home equity.

Source: Black Knight Mortgage Monitor, 2026

Commentary:

Your home is a resource—not just an expense item. For retirees, home equity can be tapped strategically (downsizing, reverse mortgages, lines of credit) to supplement income, fund healthcare, or create legacy gifts. Understanding when and how to use it is key to your personalized retirement plan.

Art and Luxury Boom Amid Turmoil

Sotheby’s London auction shattered records: $207 million in sales, nearly double last year. Every item sold.

Source: ArtNews – Record Sotheby’s Auction

Commentary:

Wealth doesn’t disappear in crises—it moves. High-end alternative assets like art and collectibles soared. While this may not be a staple for most retirees, it highlights a broader truth: in volatile times, diversification—even in alternatives—has value for certain investors.

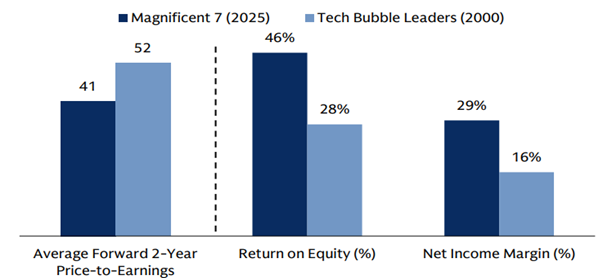

No Bubble Yet: Fundamentals vs. Headlines

Despite rising valuations, fundamentals support today’s “Magnificent 7”—very different from the 2000 tech bubble.

Source: Goldman Sachs Research – Tech Valuations 2026

Commentary:

Sound fundamentals are what you want in retirement, not speculation or hype. High-quality growth names with real earnings and cash flow may deserve a place in your plan, but prudent sizing and regular rebalancing remain key.

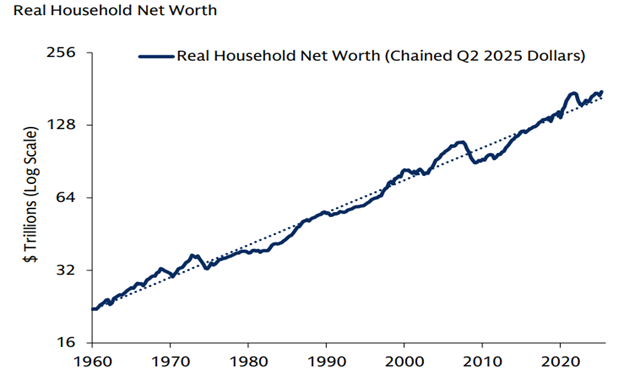

Household Balance Sheets: Stronger Than They Look

Despite $20 trillion in household liabilities, strong real net worth means debt service remains manageable for most Americans.

Commentary:

Having debt is not inherently bad—in context, strong assets can offset liabilities. Retirees should review their own balance sheets: consider reasonable use of debt (like manageable mortgages or strategic lines of credit) if it improves cash flow or reduces stress.

Final Thoughts

The more things change, the more timeless certain retirement truths become. This week’s headlines reinforce pillars essential for thriving in retirement:

- Diversification is forever in style—across sectors, geographies, and even asset types.

- Adaptation and discipline outpace hot takes and panic.

- Innovation can’t be ignored—tech and financial change, like crypto and drones, reshape everything (often faster than we expect).

- Personal finance is just that—personal. Whether it’s tapping home equity, evaluating debt, or updating your withdrawal plan, the right moves are always about your goals and values, not just the headlines.

Stay thoughtful, flexible, and focused on your path—and you’ll enjoy a retirement as rewarding as it is resilient.