JPMorgan’s new “lifestyle” service

JPMorgan Private Bank launched a lifestyle/concierge offering — discounts and curated referrals for luxury services (private jets, travel, household staff, art services, luxury goods). Entrepreneur+1

Why it matters:

High-net-worth households increasingly want consolidated convenience: travel, lifestyle, and wealth all coordinated. For you, that makes two practical points. First, luxury concierge services can save time and sometimes money — which matters when time is as valuable as money. Second, bundling lifestyle with financial services illustrates how wealth firms compete on experience, not just returns. When evaluating services, ask: does this save you meaningful time, reduce stress, or create measurable value in your retirement life — or is it just convenience wrapped in marketing?

Gold supply grows only ~1–2% a year from mining

Annual mined gold supply growth is small—on the order of ~1% (recent data shows mine production increases around 1% y/y; historical growth has been roughly 1–2% a year). Supply also depends on recycling and geopolitics. World Gold Council+1

Why it matters:

Gold’s scarcity is structural: mines don’t rapidly increase output when prices spike, so supply is relatively inelastic. For retirees considering gold as insurance for currency or debt risk, that scarcity helps explain why gold is an effective hedge in stress scenarios. But it’s not income-producing — treat it as a defensive, tail-risk insurance allocation sized modestly (often single-digit %) within a diversified plan.

In France, average retiree income now exceeds many workers’ incomes

Reporting shows average incomes for some retired cohorts in France now exceed incomes of many working-age households — a notable social and policy phenomenon. AInvest+1

Why it matters:

This illustrates two lessons: 1) national policy and benefits design can materially shift relative living standards across age groups; and 2) retirement income adequacy is partly political, not purely personal. For U.S.-based retirees, it’s a reminder to watch policy (taxes, health benefits, COLA) because public programs and political choices can change retirement economics materially over time.

Darden: casual-dining visits rose across income groups

Darden Restaurants reported same-restaurant sales and guest visits rising year-over-year across income groups — a sign of resilient consumer demand at casual dining chains. Darden Restaurants+1

Why it matters:

Consumer resilience in restaurants suggests pockets of stable spending even if broader metrics look softer. For investors and retirees relying on equity income or dividends from consumer-focused companies, examine revenue quality: are sales driven by pricing or genuine traffic growth? Traffic-driven growth tends to be more durable. In portfolio terms, favor companies with both pricing power and diverse customer bases.

Big names urging higher gold weightings

Prominent investors (e.g., Ray Dalio, Jeffrey Gundlach, David Einhorn) have publicly recommended adding gold as an insurance asset amid debt and currency concerns. Wealth Advisor+1

Why it matters:

When respected investors call gold “insurance,” they’re signaling concern about fiat risk (currency/debt) and tail scenarios. Educationally: think of gold as portfolio insurance — it can protect purchasing power under certain stress scenarios, but it won’t fund living expenses. For retirees, allocate defensively: maintain enough liquid income sources for near-term needs, and consider gold’s role as a small diversifier against extreme fiscal or monetary shocks.

Goldman raises S&P 500 year-end target (to 6,800)

Goldman Sachs raised its S&P 500 year-end target to ~6,800, reflecting views that Fed easing + strong earnings could support more gains. Reuters+1

Why it matters:

Analyst targets help form scenarios but are conditional: they assume policy moves and earnings stability. For retirees, don’t treat target moves as certainties — instead, use them as input to scenario planning (base / optimistic / conservative). That helps translate market calls into practical decisions: harvest gains for income, adjust glidepaths cautiously, and keep liquidity to cover living expenses during corrections.

Most ETF inflows are now hedged (currency hedging surge)

Analyses show over 80%

of recent inflows into some U.S. equity ETF categories are currency-hedged — a big swing from low hedging earlier in the year. Reuters+1

Why it matters:

A surge in hedged flows means global investors are more worried about currency moves (e.g., dollar swings). For U.S.-based retirees with foreign exposures, that matters because hedging choices change returns and volatility. If you hold international assets unhedged, a weaker dollar boosts returns; if you hold hedged foreign assets, you get more pure equity exposure with lower currency noise. Understand whether your international sleeve is hedged — that affects expected return and risk.

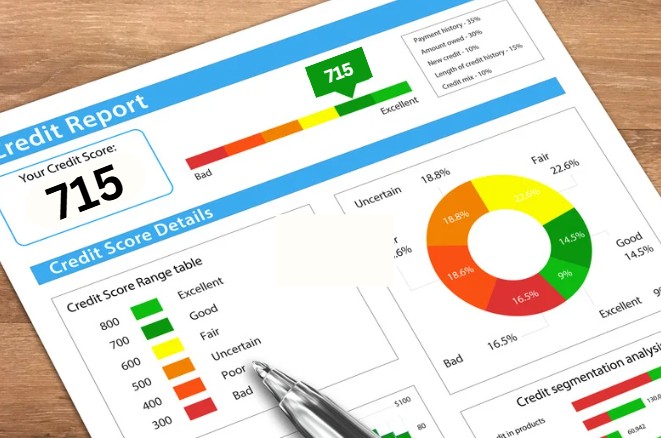

FICO scores slipping (average ~715)

The national average FICO score fell to ~715 (down from 717 a year earlier); Gen Z saw notable declines. FICO+1

Why it matters:

Declining credit scores suggest higher consumer stress — more late payments, higher utilization — which can foreshadow weaker consumer spending or rising delinquencies. For retirees, this is important in two ways: first, it affects the broader economy (consumption-driven returns); second, if you co-sign, gift, or plan to support family, their weaker credit may increase the chance you’ll be asked for help. It’s wise to include contingent family-support scenarios in your planning.

Next generation planning & inflation math

A reminder that modest inflation (e.g., 3%) can halve purchasing power over ~24 years — important for younger annuity purchasers and premium decisions. Fortune

Why it matters:

Inflation slowly erodes real income. For retirees and younger annuity buyers alike, inflation assumptions directly affect how much income is needed. Educationally: when choosing annuity options, compare inflation-adjusted riders vs. nominal payouts, and model real purchasing power across decades. For those with $1M+, small premium differences can compound into material income gaps over time.

Market breadth still narrow (few stocks at 12-month highs)

Market indices are setting highs while breadth is narrow — fewer than 1 in 10 stocks are at 12-month highs in some readings, meaning gains are concentrated. Yahoo Finance+1

Why it matters:

Narrow leadership raises concentration risk: if a handful of companies reverse, index returns can fall quickly. For retirees, concentrated-market rallies increase tail risk. Educationally: emphasize diversification beyond headline indices (sector, size, geography) and consider rebalancing or trimming concentrated winners to lock in gains for income needs.

JPMorgan warns visa fee changes could reduce ~5,500 work authorizations/month

JPMorgan economists modeled that a proposed steep H-1B fee increase could cut about 5,500

work authorizations per month — with potential implications for hiring and innovation. Bloomberg+1

Why it matters:

Workforce policy shapes productivity and corporate earnings over time — tech and services firms rely on skilled foreign labor. For portfolio and retirement planning: reduced labor supply could raise wage pressure in certain sectors, impact profit margins, or slow growth in innovation-driven companies. It’s another reminder to include policy and labor dynamics within long-term return expectations.

Final Thoughts

Taken together, these items paint a consistent educational picture for high-net-worth pre-retirees and retirees:

- Risk is multi-dimensional. Market risk (narrow breadth, high valuations), policy risk (visa fees, COLA, benefits), and non-market risk (cybercrime, health trends) all matter. Good planning recognizes and layers protections across these risks.

- Insurance and diversification matter more now. Gold’s rise, hedged ETF flows, and calls from big investors for insurance assets highlight that adding defensive, non-correlated pieces (small gold allocation, diversified international exposure, inflation-protected income) can materially improve resilience.

- Behavioral and household risks are real. Credit-score dips, renter burdens, and family support expectations mean advisors should model contingencies (family support scenarios, cash buffers) — not just market returns.

- Opportunity still exists — but be conditional. Analysts’ bullish targets and corporate resilience point to upside, but those outcomes depend on policy and earnings staying favorable. Translate market optimism into actionable rules: harvest gains when appropriate, keep a multi-year liquidity buffer, and avoid overconcentration.

- Make planning concrete, not theoretical. For a household with $1M+ investable assets, the practical next steps are straightforward: update scenario tests for COLA, health-cost inflation, housing support to family, and longer lifespans; confirm how much of your portfolio is earmarked for durable income vs. optional growth; and add simple non-market protections (cyber monitoring, identity protection, small gold/hedge allocation) where they reduce tail risk.